Bursar Bulletin: MAGA Accounts vs 529 Plans - what's the difference?

The House just passed the 'One, Big, Beautiful Bill', and with it, a brand-new rival to the classic 529. MAGA accounts are here - and yes, parents will come asking. Consider this your cheat sheet.

Spring has well and truly sprung. Memorial Day weekend has passed, the days are getting warmer, and, if you’re like me, allergies are finally starting to subside.

With all that comes the unavoidable fact that Fall tuition isn’t all that far away, and the “questions, concerns, and comments” will come in thick and fast from student families in no time at all.

As I’ve spoken about (at length - I know), my bet is everyone reading this is going to have a record number of 529 payments this semester - a continuing trend of the acceleration of 529 payments as a percent of total tuition payments. Of course, this always leads to the inbound of “what do I do with this 529?” or “have you got my check yet?” - particularly from Freshmen parents. But this semester, you might also get some questions about a new kid on the block - and by new kid, I mean the MAGA Savings Account that was passed by the House as part of the One, Big, Beautiful Bill.

What is a MAGA Account?

Section 110115 of the bill establishes “Money Accounts for Growth and Advancement” (MAGA accounts), a new type of savings vehicle designed to promote long-term investments in education, entrepreneurship, and homeownership.

Here is a quick-fire summary in FAQ form:

1. Who can open an account?

Parents can open a MAGA account for any U.S. citizen child under age 8 (starting in 2026) and contribute up to $5,000 per year in after-tax dollars.

2. How much can be contributed each year?

Contributions from taxable persons (i.e. parents, grandparents, crazy uncles etc.) are capped at $5,000 annually (inflation-indexed)

However (and this is a cool one) contributions from tax-exempt entities (like foundations or nonprofits) are allowed above that limit if made available to all children in a defined group. I will come back to this as I think this is one of the better components of the MAGA account concept.

3. What are the tax advantages?

Funds in a MAGA account grow tax-deferred, and withdrawals are restricted by age and purpose:

No distributions allowed before age 18.

At 18, 50% of the account balance can be used for qualified purposes like higher education expenses, certified training programs, starting a small business, or first-time home purchase.

At age 25 the beneficiary can use up to 100% of the account for those qualified purposes, and by age 30 funds can be withdrawn for any purpose.

Distributions used for the approved educational or advancement purposes are taxed at long-term capital gains rates (generally lower than ordinary income tax), whereas withdrawals for non-qualified purposes (after age 30) are taxed as ordinary income

4. Does the government contribute anything?

For every U.S. citizen child born between January 1, 2024 and December 31, 2028, the government will contribute $1,000 into a MAGA account opened for that child.

Parents or guardians must open the account (both parents must provide work-eligible SSNs to qualify) and if they don’t do so by the time they file the first tax return claiming the child, the Treasury is authorized to create an account on the child’s behalf.

This essentially functions as a federal seed money program to jump-start college or future opportunity savings for children - quite similar to a “baby bond” focused on education and personal advancement.

How do they compare to 529?

Every good piece of analysis always comes with a caveat - and mine here is that we really don’t have that much in the way of details about the MAGA account. A lot of guidance around how these things actually work in practice usually come after the fact, and through things like IRS guidance documents, which are likely years away for MAGA accounts (assuming they are still part of the bill post senate vote).

However, I think it’s always worth doing a bit of a comparison with the data we do have as of today - so here is my attempt at a summary of the key differences.

What are the impacts?

My opinion is that any time families get broader access to savings instruments, particularly when it focuses on things like education or starting a business, I am generally all for it. In this way I really don’t think it needs to be an either-or thing between MAGA and 529, but rather what makes the most sense first, and in which situation.

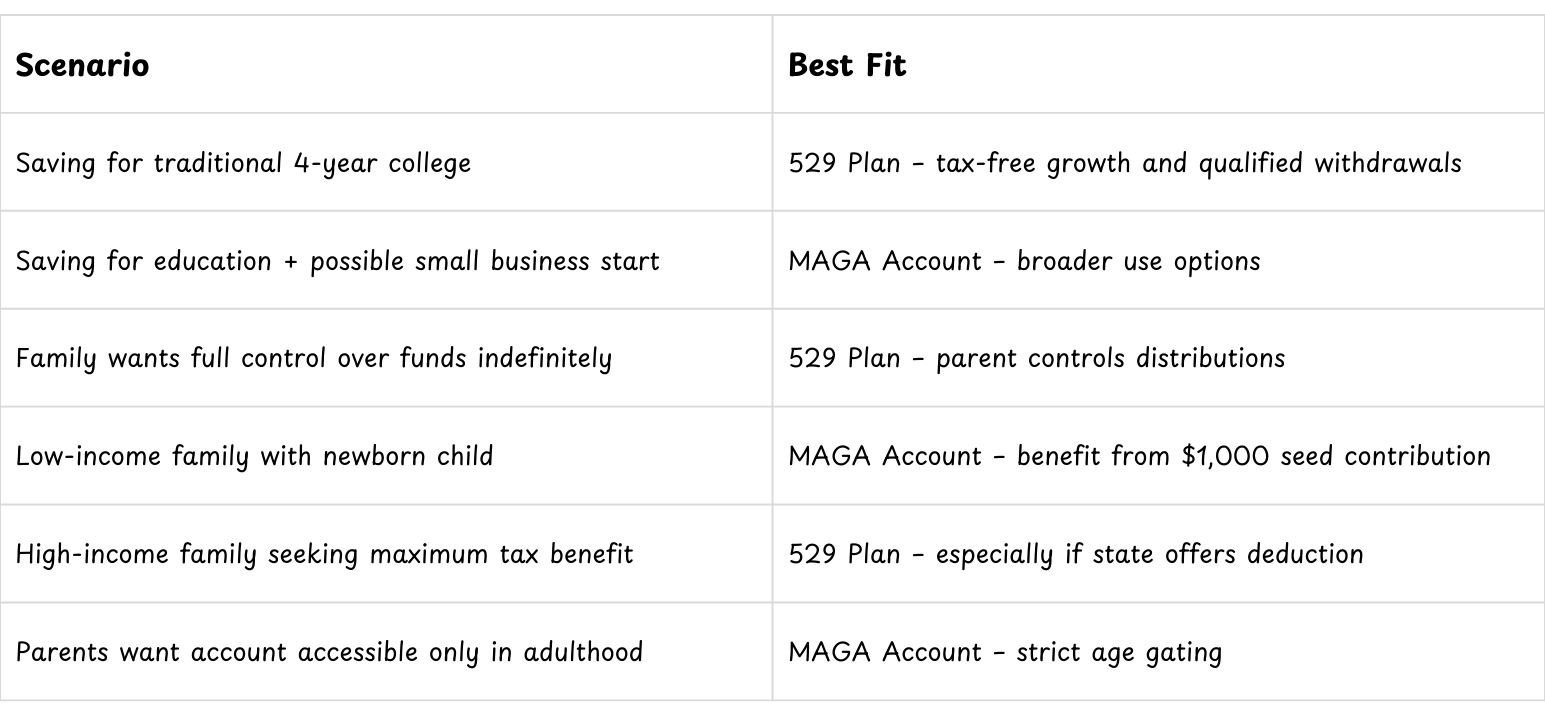

Here are some extremely broad, hypothetical scenarios to give you a sense of where I think different savings instruments can be helpful for different reasons.

There are a few open questions, though, and I am hopeful that a lot of these will get answered over time, and answered in a way that truly does make the addition of the MAGA account a helpful expansion of tools available to families.

FAFSA Calculations: 529 plans currently get fairly favorable treatment in FAFSA assessments. It is yet to be clarified how these MAGA accounts would be treated (though we have quite a while to clarify).

529 Legislative Expansion: There are a number of bills currently out there looking to expand the usefulness of 529 Plans; a really great thing given the tax-advantages are massive (and actually bigger than MAGA accounts). This includes the School Choice Legislation Prioritizing the Right to a Quality Education for Every Child bill introduced by Ted Cruz earlier this year. My sincere hope is that these efforts don’t get stalled or stopped because of the introduction of MAGA accounts.

529 Awareness: If the goal is to save for education, the 529 account is simply very hard to beat. However, a recent study from Edward Jones showed that over half of all Americans still don’t know what a 529 account is, and only ~14% have or plan to use a 529 account as part of their education savings strategy. My hope is that MAGA accounts are supplementary and do not replace awareness; and to be an external optimist - perhaps MAGA accounts being in the news actually raise awareness further for 529 plans!

What else happened this week?

Stablecoins continue their insane upward-trajectory around the globe:

Kraken, a cryptocurrency exchange similar to Coinbase, is releasing tokenized securities of stocks like Apple, Tesla and Nvidia. This will allow them to be traded more freely (24/7), though it has its own hurdles. Read more here.

The UK government has unveiled new legislation to establish "consistent standards" for buy now, pay later (BNPL) firms and protect shoppers against "racking up unaffordable debt", according to a statement from the Treasury. Read more here.

That’s all for this week folks! Hope everyone had a fantastic long weekend.

See you all next week.

Cal