Bursar Bulletin: Major aid shakeup from House reconciliation will impact students in 2025/26

The Student Success and Taxpayer Savings Plan outlines huge changes to Pell Grants, Eligibility, Student Loan Caps, as well as introduces risk-sharing models into the Higher Ed system.

After last week’s newsletter, we had a few people ask about a similar summary for the changes that will be going into effect as a result of the House Committee on Education & Workforce Student Success and Taxpayer Savings Plan.

A lot of you might remember the College Cost Reduction Act (“CCRA”), though it didn’t end up going into effect after it didn’t get enough votes in the House (and perhaps heaved a sigh of relief just given the amount of changes in there!).

Well, a lot of the elements of that bill have now been reintroduced through the reconciliation process, and have ended up in the Student Success and Taxpayer Savings Plan. While not all changes will impact the 2025/26 academic year, some will, and this fall is probably a good time to be communicating the components that will go into effect next year!

My plan is to:

Give a bit of a summary of everything (which is no small feat!)

Highlight the critical changes, particularly those that go into effect for this year

Brainstorm some actionable takeaways you can build on with your team!

Provide a more detailed comparison of the old vs the new - a cheat sheet for you

My attempt at a summary…

What happened?

In late April, the House Committee on Education & Workforce advanced the Student Success and Taxpayer Savings Plan, a reconciliation bill proposing arguably the most dramatic reshaping of federal aid since the Higher Education Act itself.

These changes aim to reduce federal spending by ~$350 billion over the next decade.

What are the big changes?

There are four big areas of change:

Changes to the Pell Grants program and Campus-Based Aid

Changes to the Federal student loan program

Institutional Accountability

Regulatory Rollbacks

Here is a summary view of the major changes under each of these categories

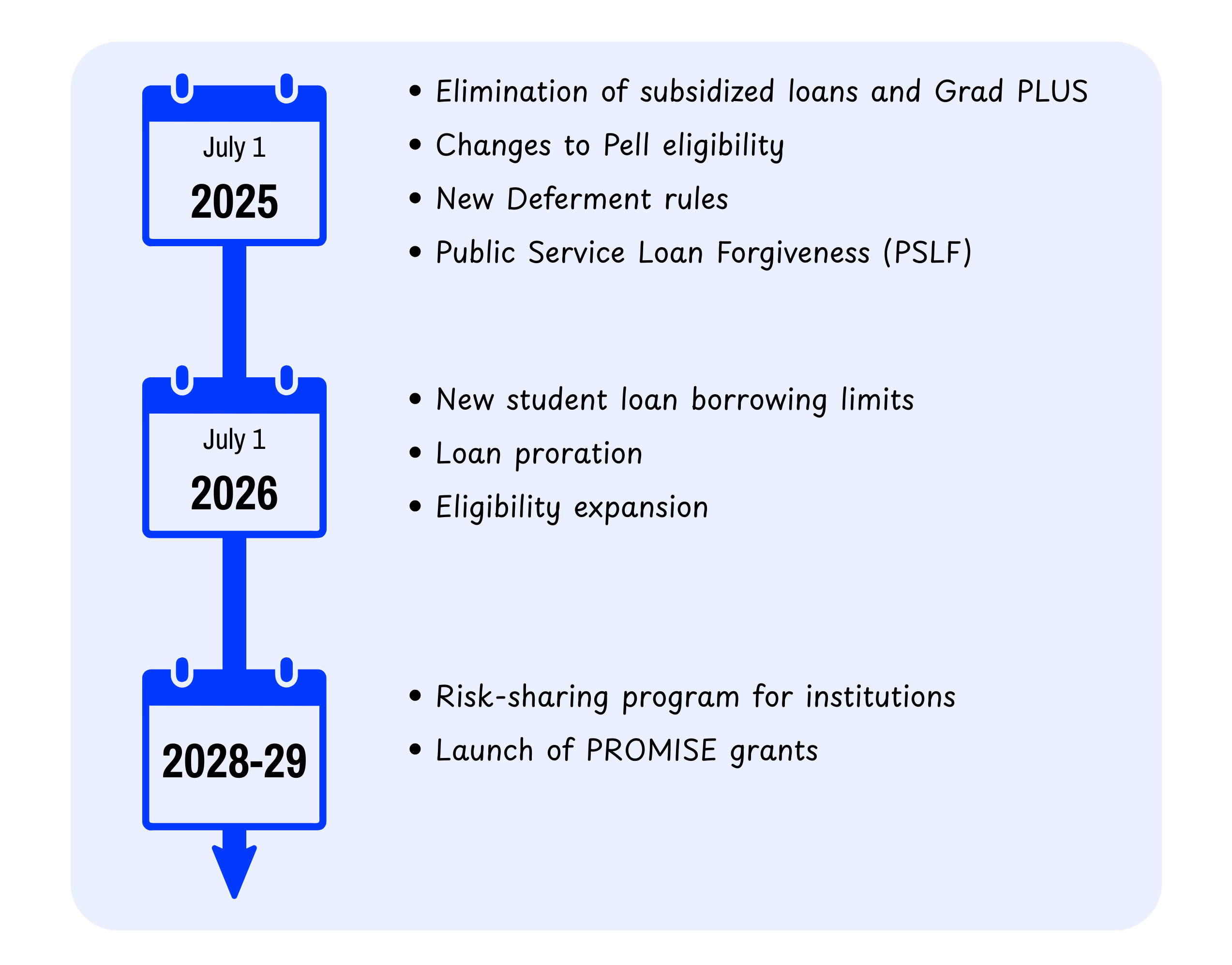

#1 Pell Grants, Campus-Based Aid & Eligibility Changes

Rules around qualification have been narrowed

Only lawful permanent residents, Cuban-Haitian entrants, certain Ukrainian and Afghan parolees, and citizens of Micronesia, the Marshall Islands, and Palau would remain eligible for Title IV aid.

Refugees, Asylees, and Human Trafficking Victims are excluded from new eligibility definitions (will see if guidance gets updated here).

Needs analysis calculation has been overhauled

New Calculation Formula: Need would be calculated as the Median Cost of College (MCOC) minus the Student Aid Index (SAI) minus other aid. This cap could limit institutional flexibility in awarding their own aid.

“Pellionaire” Crackdown: Students with high assets (SAI > 2× max Pell) will be barred from receiving the grant, regardless of income.

Eligibility for Pell Grant has been tightened

30-Credit Requirement: Full-time Pell eligibility raised to 30 credit hours/year (from 24). Less-than-half-time students lose eligibility entirely.

Workforce Pell: New short-term Pell for students in 150–600 clock hour programs aligned to in-demand jobs (launching 2026–27).

Introduction of the PROMISE Grant

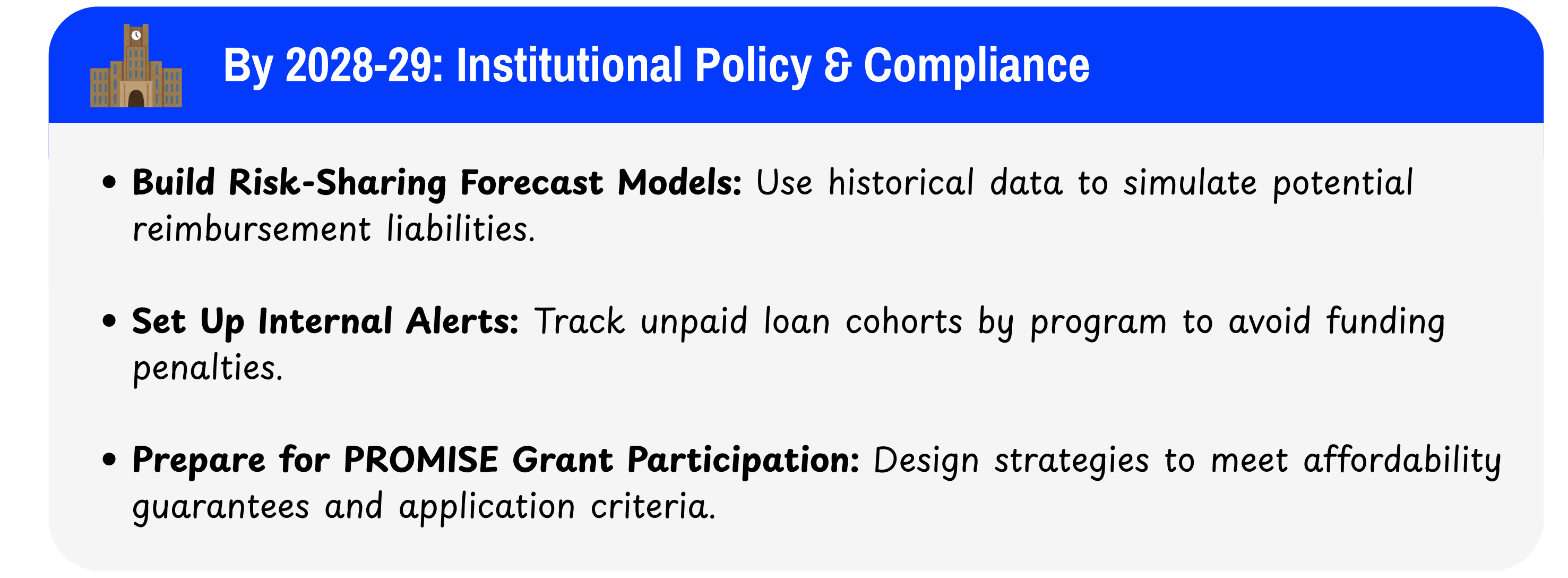

New campus-based aid program, funded by institutional reimbursements for unpaid loans, starting 2028–29. Tied to affordability metrics and performance guarantees.

#2 Changes to the Federal Student Loan Program

Loan program changes and caps

No More Subsidized or Grad PLUS: Both eliminated after July 1, 2026.

Major changes to federal borrowing caps:

Undergraduate Students: Lifetime borrowing capped at $50,000.

Graduate Students: Lifetime borrowing capped at $100,000.

Professional Degrees (e.g., JD, MD): Lifetime borrowing capped at $150,000.

Parent PLUS Loans: Limited to $50,000 per child, replacing the previous allowance up to the full cost of attendance.

Annual Loan Caps: Based on median cost of the student’s program, minus Pell. Proration required for part-time students.

Loan repayment changes

Repayment Assistance Plan: Single income-driven repayment option. Forgiveness after 30 years, with an interest subsidy and limited principal relief. Borrowers locked into this plan once selected.

Streamlining of repayment options:

The current array of repayment options will be consolidated into two:

Standard Tiered Repayment Plan:

Repayment terms based on loan balance:

Under $25,000: 10 years

$25,000–$50,000: 15 years

$50,000–$100,000: 20 years

Over $100,000: 30 years

Minimum monthly payment: $10

Income-Driven Repayment (IDR) Plan:

Payments range from 1% to 10% of adjusted gross income, with a $50 deduction per dependent child.

Forgiveness eligibility after 30 years of qualifying payments, extending from the previous 20–25 years.

Deferment & Forbearance Cutbacks: Unemployment and economic hardship deferments eliminated for new loans (post-July 2025). Forbearance capped at 9 months per 24 months, with narrow exceptions.

PSLF has been trimmed

Internship Exclusion: Medical/dental internships or residencies will not count toward PSLF unless the borrower already has eligible loans as of June 30, 2025.

#3 Institutional Accountability

Introduction of risk-sharing; placing ‘skin-in-the-game’ for universities

Starting 2028–29, schools must reimburse ED for a portion of unpaid Direct Loans issued after July 2027.

Amounts vary by cohort: based on value-added earnings for completers and completion rates for non-completers.

Noncompliance Penalties: Institutions can lose loan and Pell eligibility if payments are delayed beyond 12–24 months.

PROMISE Funding: These reimbursements will fund the new PROMISE Grant program.

#4 Regulatory Rollbacks

Rollback of a number of regulations previously introduced

Goodbye, 90/10 Rule: Fully repealed.

Borrower Defense & Closed School Discharge: Reverts to pre-2022 rules.

Gainful Employment: Legal references removed, effectively ending GE authority. FVT regulations remain untouched - for now.

ED Power Curbed: Education Department barred from creating similar regulations unless explicitly authorized by Congress.

When does everything go into effect?

Here’s the fun part! There are some pieces that come into effect July 1st of 2025 (aka less than a month!), some parts that come into effect in July 2026, and some that will launch in 2028-29. Here’s a bit of a visual to give you an idea:

An action plan for Bursar and Financial Aid Offices

This is an absolute doozy of a legislation change just given the breadth of changes - impacting both Financial Aid and Bursar offices - but also because of the staggered timing. It does mean that some readiness actions need to be taken near-immediately, while some are longer-term. A lot of this is also going to impact at the CFO level, and a great opportunity to help the broader finance department plan for things like the risk-sharing liabilities!

I put together a framework that hopefully gives you a starting point - but nothing beats getting in front of a whiteboard with your team and brainstorming your own action plan heading into this fall semester!

The nitty-gritty details

There are a crazy amount of details and nuances to this proposal - too many to go into enough detail on in this format (at least not without boring you to death, or losing a few hundred subscribers).

Having said that, I wanted to spend the time to create a Comparison Fact Sheet for you all, summarizing the major policy changes, the comparative rules in existing law, and some notes on the intended impact of the change.

Here is the link to download the Fact Sheet (PDF).

If you find this helpful, please do let me know - it takes a good amount of time to go through everything to pull these together, but if they are helpful than I will keep doing them as new legislation or technologies pop up!

What else happened this week?

Perplexity and PayPal have teamed up for in-chat, AI-powered shopping. U.S. consumers will soon be able to book travel, buy products and secure concert tickets on Perplexity’s chat interface, paying instantly with PayPal or Venmo. Read more here.

Side note: I think universities will need to accept these types of alternative payments very soon, and we are working on that at Backpack!

Perplexity (big week for them) also launched Perplexity Labs, which is essentially an AI designed to help you build apps for projects. Have a look through some of the projects out there - it’s very cool stuff.

Monarch Money, a personal financial management tool raised a $75M Series B. I actually happen to use Monarch and it’s fantastic - but the more interesting part is that consumer fintech has been struggling recently, and this is a bit of a violation of that narrative! Read more here.