Bursar Bulletin: Cash App's poor performance - a canary in the coal mine?

Cash App's consumers are spending less - this might mean trouble to come for the American consumer. Plus, FedNow releases their Q1 '25 metrics.

Is Cash App’s poor earnings release a canary in the coal mine for consumer spending?

Consumer spending is always such a big talking point in the economic world, though is also so difficult to pin down. Most consumer spending metrics are fairly backward looking and often get revised - making it very difficult to pin down what is actually happening. Sometimes though, we do get a ‘canary in the coal mine’ type event.

What happened?

Cash App’s parent company, Block, reported a very underwhelming earnings report this week, leading to a 20% plunge in their stock price - their second-worst trading day in their history.

Why is this a big deal?

Usually a bad day for a single fintech stock isn’t much to write home about; however, this one is particularly interesting because of what drove the weaker than expected performance.

Cash App primarily serves lower-middle income Americans who have historically been more sensitive to changes in economic conditions - and are often the first ones to display changes in consumer spending patterns. ~95% of Cash App’s gross profit miss was driven by “softer inflows and Cash App card spend” - in other words, their customers started spending dramatically less in Q1 2025 versus Q4 2024.

Is this relevant for the Bursar Office?

I really think it is. Any data that might give us insight into the state of affairs of the average American consumer is important as we think about the incoming Fall semester. Everything from enrollment rates to payment plan delinquencies are impacted by the state of the consumer, and while this is only one potential indicator, it is definitely something to keep abreast of.

I spoke about this last week too, but the economic volatility and (potential) downward trend in consumer confidence/spending could really impact University cashflows this coming semester. Having strategies and controls in place to ensure it doesn’t break university budgets.

👉 Read more here.

FedNow posts impressive growth - the continued shift to real-time payments

Those die-hard Bursar Bulletin readers out there (I like to think they exist 😉) might remember that one of my first newsletters was about the rapid adoption of FedNow, the real-time payments capability the Federal Reserve released a couple of years ago.

It is a really exciting development because FedNow represents a faster secure version of ACH while still maintaining the cost and security benefits relative to methods like wire or credit and debit cards.

What happened?

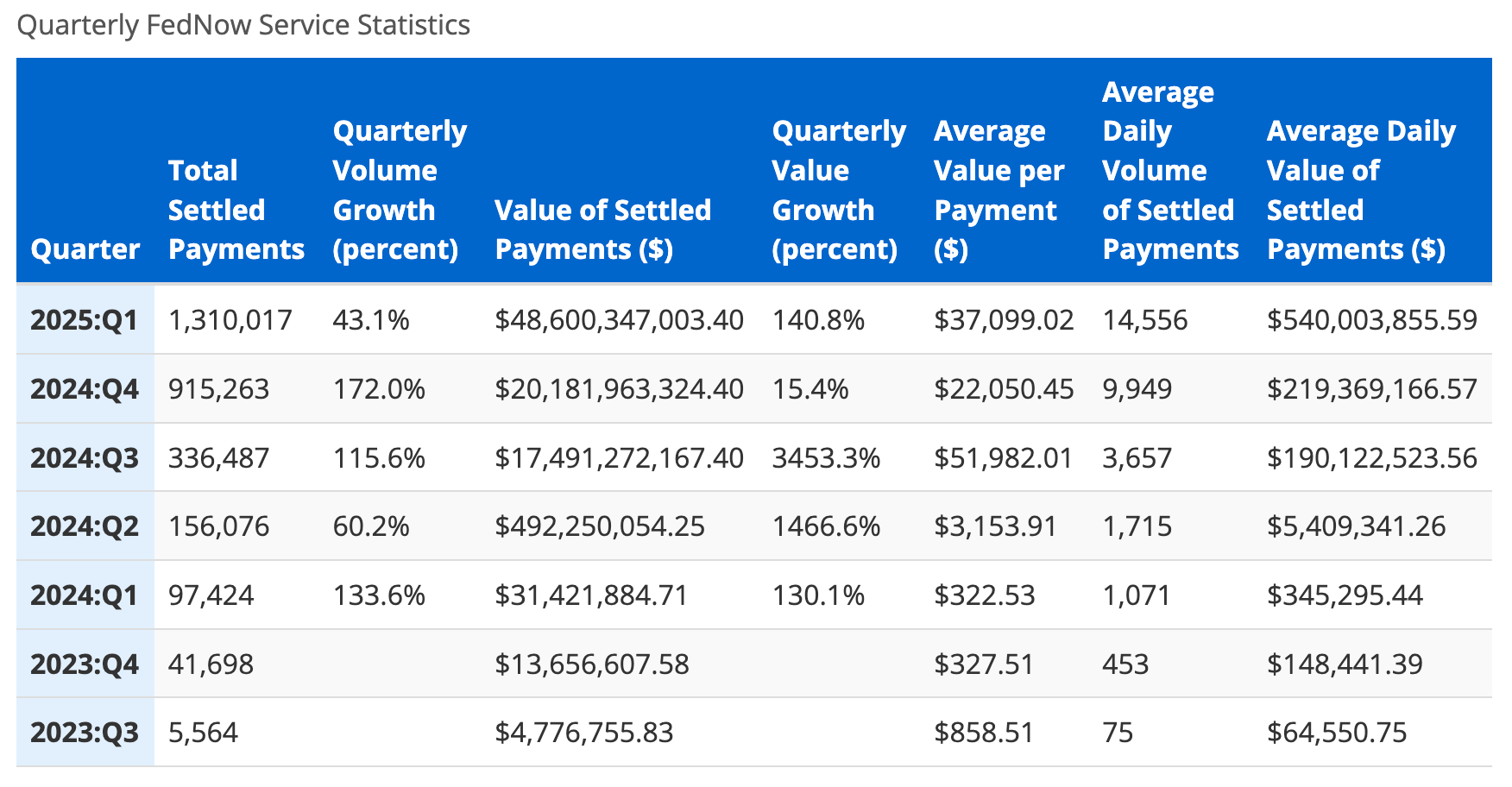

FedNow posted their Q1 2025 metrics, and in short - they were pretty impressive. A couple of highlights:

1.3M+ payments processed

$48.6B in money moved (+140% vs last quarter)

More than 1,300 participating financial institutions headquartered in all 50 states.

Small and midsize financial institutions, including community banks and credit unions, make up more than 95% of participants on the network.

What does FedNow give us?

✅ Instant access to cash flow — no more waiting days to settle

✅ Safer, faster payouts for businesses and consumers

✅ 24/7/365 infrastructure — not tied to bank hours

✅ A modern, more inclusive payment rail

If you are interested in learning a little more, the Federal Reserve has created an Instant Payments University that explains the ins-and-outs of their instant payments technologies and developments.

That’s it for this week, folks! The team and I will be out in Ohio later this week for the Ohio Bursar Association Conference, and in Santa Barbara the week after for the PacWest Bursars Conference. Hope to see many of you there!

See you next week.

Cal